Acorns

Invest spare change

One of the leading voices and biggest success stories in the FIRE movement — short for “financial independence, retire early” — Grant Sabatier has amassed enough money to live comfortably off income from his investments.

Sabatier views his situation as the end goal for people who think about money the way he does: not as something that allows you to buy things, but as a means of giving you more choices in how you want to live.

“With every dollar you save, you give yourself more freedom and options in life,” he said. “Based on how much you have saved and invested, ask yourself, ‘How many months of freedom have you acquired?’”

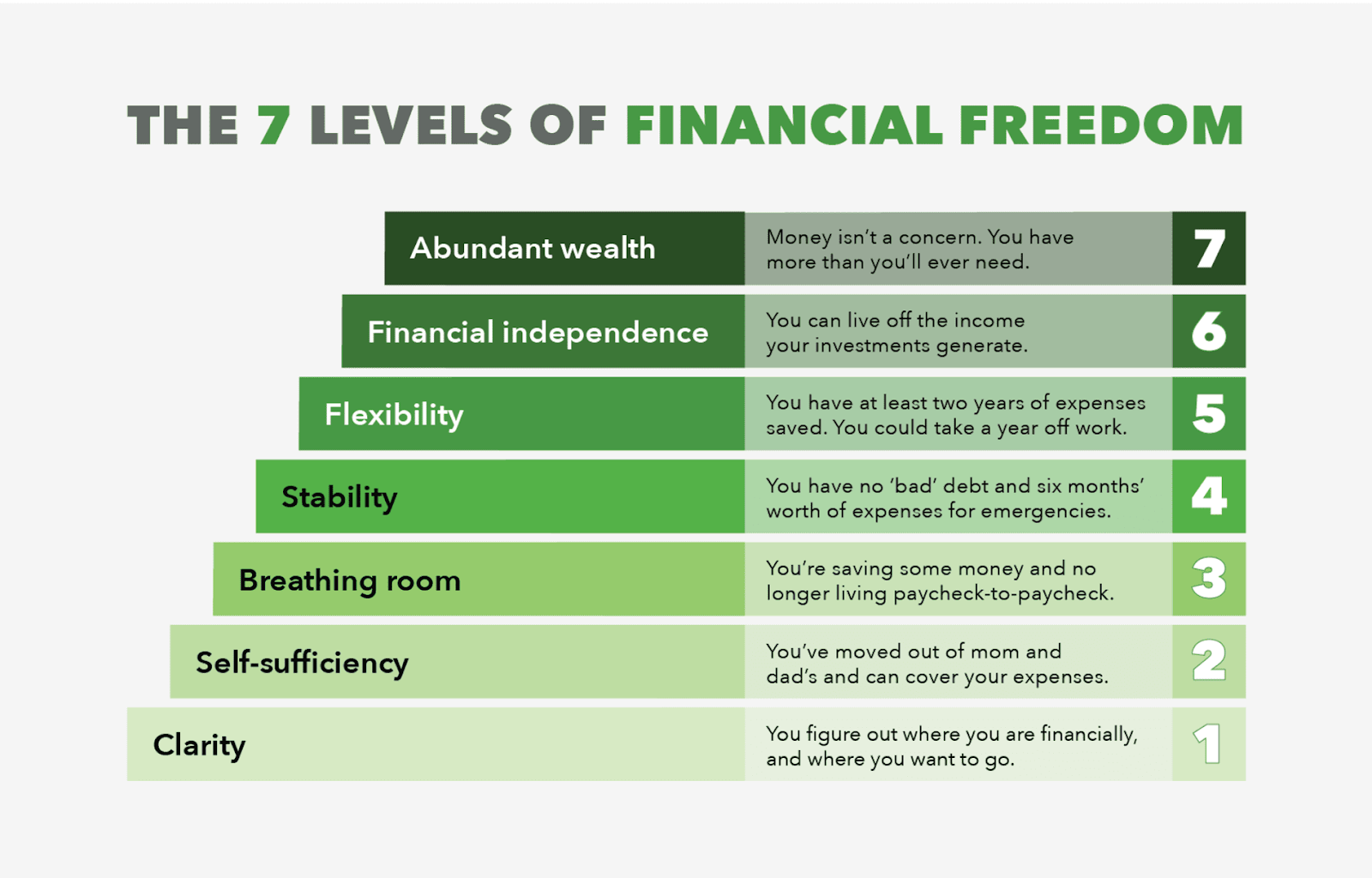

Sabatier has spent post-9-to-5 life in what he calls “a mission-driven phase.” In his book “Financial Freedom,” Sabatier offers a roadmap to money security which includes seven levels of financial freedom.

Half of working Americans say they live paycheck to paycheck, according to a 2022 MagnifyMoney survey, which puts them at Level 2, self-sufficiency.

Progressing through the levels likely requires a shift in your financial habits and overall thinking around money, Sabatier says.

The first step is taking stock of your financial situation — how much money you have, how much you owe, and what your goals are. “You can’t get to where you want to go without knowing where you’re starting from,” Sabatier says.

Next, you’ll want to be standing on your own two feet, financially speaking. This means earning enough to cover your expenses without any outside help, such as contributions from Mom and Dad.

At this level, Sabatier notes, you may be living paycheck-to-paycheck or taking on loans to make ends meet.

People at Level 3 have money left over after living expenses that they can put toward goals such as building an emergency fund and investing for retirement.

Escaping Level 2 means giving yourself some financial leeway, which Sabatier notes doesn’t necessarily mean making a much bigger salary. Indeed, 31% of working Americans making over $100,000 live paycheck-to-paycheck, according to the MagnifyMoney survey.

Those who reach Level 4 have paid down high interest rate debt, such as credit card debt, and have stashed away six months’ worth of living expenses in an emergency fund. Building up emergency savings helps ensure that your finances won’t be thrown off track by unexpected circumstances.

“At this level, you’re not worried if you lose your job or if you have to move to a different city,” Sabatier says.

When calculating how much you’d need to have saved, think about what your financial picture might look like in an uncertain financial moment, rather than just factoring in your regular, everyday expenses, financial experts say.

“If you have a job loss, you’d make some changes. You’d probably cut your gym membership and get rid of your subscriptions, for instance,” Christine Benz, director of personal finance and retirement planning at Morningstar, told Grow. “Think about the bare minimum you’d need to get by.”

People at Level 5 have at least two years’ worth of living expenses saved. With those kinds of savings, Sabatier suggests, you have the ability to think about your money in terms of the time it can buy you: “You could take a year off from your job if you wanted to.”

You needn’t carry all of this money in cash, Sabatier notes: it could be a sum total from your savings and investment accounts. As long as you’re able to access that money somehow, if you need it, you have the flexibility to untether yourself, at least temporarily, from the workforce.

People who have achieved financial independence can live solely off the income generated from their investments, according to Sabatier’s framework.

“You generally have one of two things,” says Sabatier. “You either have a large pile of money in an investment portfolio that’s generating interest, or you have rental properties, and cashflow from the rent covers your living expenses, or a hybrid of the two.”

To get here, you’ll likely have to invest a high percentage of your income, which could require you to shift to a more modest lifestyle to drastically lower your cost of living. Pursuing this lifestyle requires a change in thinking, Sabatier says.

Financially independent folks who live off their portfolio income often rely on the “4% rule” — a retirement rule of thumb that posits that an investor can safely withdraw 4%, adjusted for inflation, from a balanced portfolio of stocks and bonds each year, and be relatively certain that the money will continue to grow and won’t run out.

Although economists debate whether 4% is the optimal number (some more conservative observers think the right figure might be closer to 3.3%), the calculation behind it serves as the basis for establishing a FIRE number — the amount of money you’d need to retire and earn an annual income you could comfortably live on.

While those in Level 6 need to monitor swings in their portfolio to make sure their retirement is still going according to plan, those in Level 7 theoretically have no such worries. “Level 7 is abundant wealth — having more money than you’ll ever need,” Sabatier says. “You don’t have to worry about money, and it’s not essential to your day-to-day existence.”

The views expressed are generalized and may not be appropriate for all investors. Investing involves risk, including the loss of principal. Carefully consider your financial situation, including investment objective, time horizon, risk tolerance, and fees prior to making any investment decisions.

This material has been presented for informational and educational purposes only. The views expressed in the articles above are generalized and may not be appropriate for all investors. The information contained in this article should not be construed as, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy or hold, an interest in any security or investment product. There is no guarantee that past performance will recur or result in a positive outcome. Carefully consider your financial situation, including investment objective, time horizon, risk tolerance, and fees prior to making any investment decisions. No level of diversification or asset allocation can ensure profits or guarantee against losses. Article contributors are not affiliated with Acorns Advisers, LLC. and do not provide investment advice to Acorns’ clients. Acorns is not engaged in rendering tax, legal or accounting advice. Please consult a qualified professional for this type of service.

Ryan Ermey was a senior reporter for Grow.